There’s a new North American free trade agreement – the United States-Mexico-Canada Agreement or USMCA – and automakers, suppliers, and policymakers are trying to digest the 1,800+ pages of text released by the U.S. Trade Representative on 30 September 2018. While there is a lot that is different in this new agreement about automotive trade, there are some things that remain the same. It is also important to keep in mind that while the text offers greater certainty about the future of North American automotive production, trade, and investments, the USMCA still must be signed, ratified, and the enabling legislation must be passed in each of the three countries before the agreement can go into effect on the target date of 1 January 2020.

What has not changed?

A few significant things did not change between NAFTA and the USMCA. Importantly, there is still a tri-lateral trade deal, and there are specific rules of origin (ROO) for automotive and automotive parts trade. Some other parts of the original NAFTA remain mostly intact including the dispute resolution mechanism known as “Chapter 19” (now Chapter 31).

What has changed?

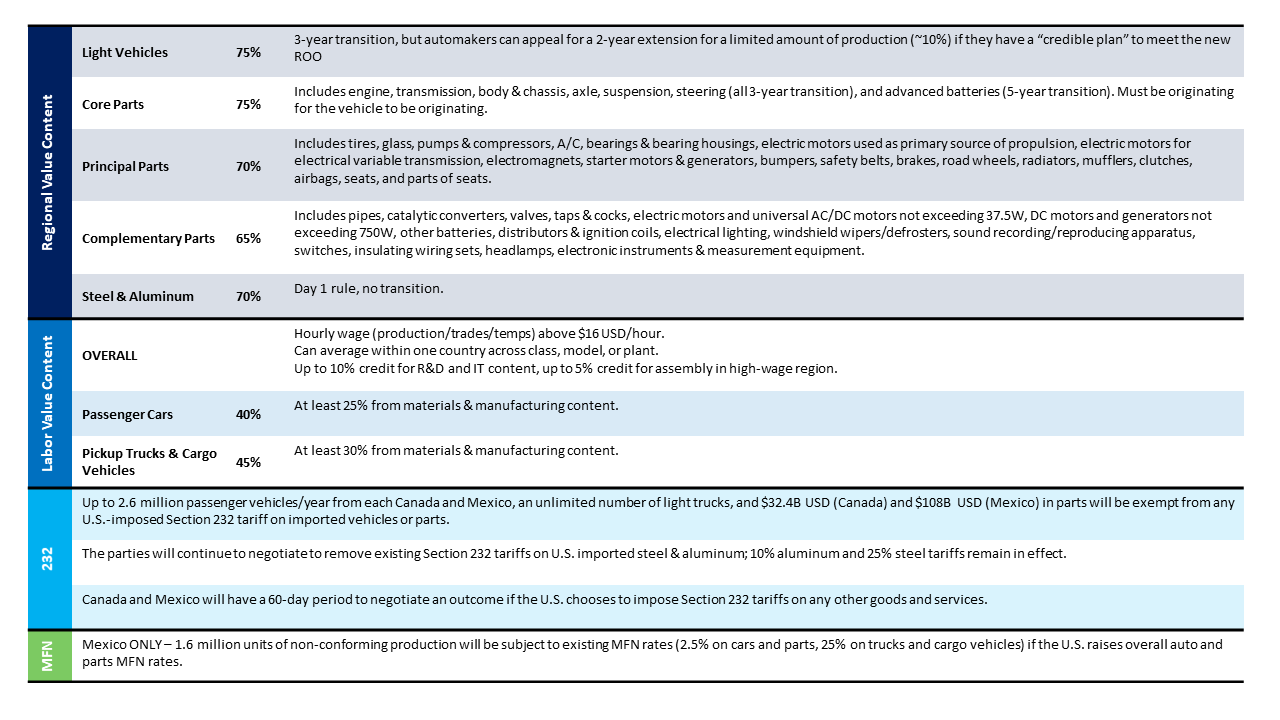

Instead of the 62.5 percent North American content hurdle in NAFTA, the USMCA sets forth a regional value content (RVC) threshold for vehicles and three categories of automotive parts: core, principal, and complementary. There is a new RVC for North American steel and aluminum content and a new labor value content (LVC) rule that states that 40 percent of a passenger vehicle and 45 percent of a pickup or cargo vehicle must be made by hourly workers who earn a wage of USD 16/hour or more. Automakers can earn up to 10 percent credit toward the LVC from R&D and information technology work done in the region where the production takes place, and a 5 percent credit toward the LVC for assembling the vehicle in a high-wage region in North America. See Figure 1 below.

Figure 1: Summary of USMCA Automotive Provisions

Source: CAR analysis of USMCA text

Canada and Mexico also negotiated side letters that mostly exempt light vehicle and parts exports to the United States from potential national security tariffs under Section 232 of the Trade Expansion Act of 1962. Canada and Mexico can each send up to 2.6 million vehicles to the U.S. market without incurring Section 232 tariffs if the United States imposes these tariffs. There is no limit on the number of trucks that the countries can export to the U.S. market, and parts exports are limited to USD 32.4B for Canada and USD 108B for Mexico. For comparison, 2017 U.S. parts imports from Canada were USD 15.8B and from Mexico were USD 53.1B. Mexico also negotiated provisions that exempt USMCA non-conforming automotive exports from any increases in the U.S. Most Favored Nation (MFN) tariff rates that the U.S. must offer to all members of the World Trade Organization. Under this provision, up to 1.6 million vehicles that do not meet the USMCA ROO, RVC, or LVC will be grandfathered in at the current 2.5 percent tariff rate for passenger cars and automotive parts and 25 percent tariff for pickup trucks and cargo vehicles. The Mexican government announced that 32 percent of that country’s current vehicle output does not conform to the new USMCA rules – about 780,000 vehicles, well under the 1.6 million cap.

What happens next?

Canadian, Mexican, and U.S. leaders are expected to sign the USMCA while attending the G20 summit in Buenos Aires in November 2018. Signing the agreement is an essential step before the deal can be entered into force, but much more must be done in each of the three countries before the USMCA can become law.

In Mexico, the legislative process to ratify the deal and enact the enabling legislation is expected to be quite quick. The deadlines to notify the U.S. Congress of the agreement on 31 August 2018 and release the text of the agreement on 30 September 2018 were all aimed at getting the USMCA approved by outgoing Mexican President Enrique Peña Nieto who leaves office on 1 December 2018.

In Canada, the USMCA must be approved by the Cabinet and considered by the Parliament, which is comprised of the House of Commons, the Senate, and the Sovereign. The Parliament will make necessary legislative and regulatory changes, and the deal must receive “royal assent” (approval by the Governor General). The only hard timeline in this process is that the House of Commons must sit with the agreement for 21 days of consideration and debate before moving forward. Canada holds federal elections in October 2019 – so for USMCA to go into effect on 1 January 2020, Canada will likely have to complete the ratification process before the election.

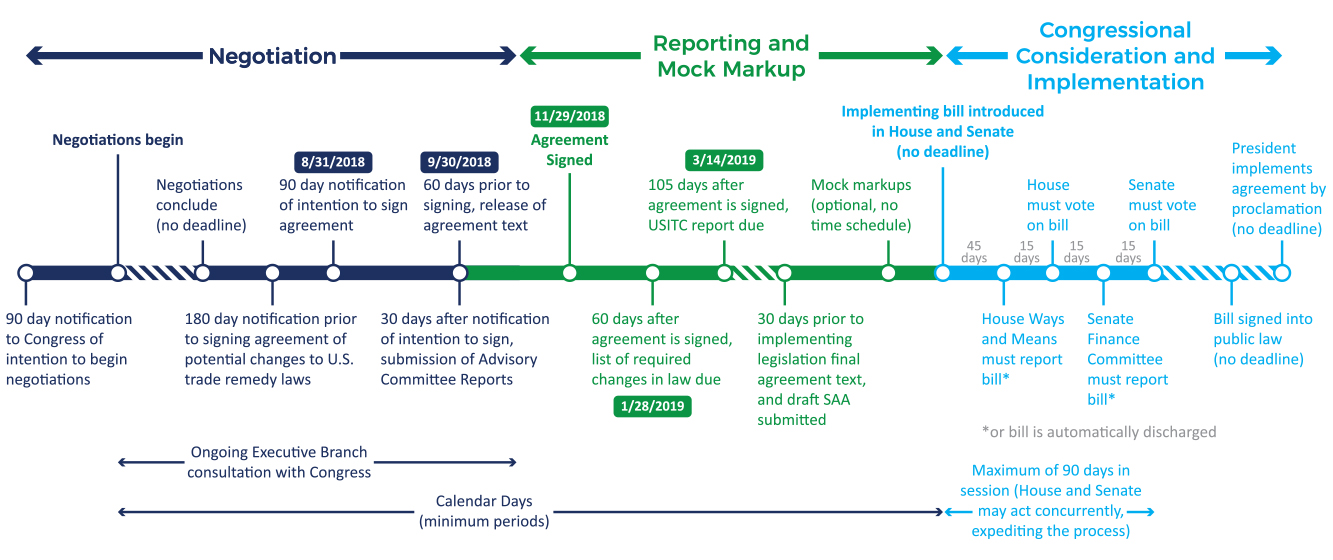

In the United States, the Congress is considering the USMCA under the Trade Promotion Authority (TPA) rules which set out milestones that are required to “fast track” the legislation (receive an up/down vote in the Congress without amendments). Figure 2 below shows the timeline. A critical milestone is that the TPA requires a report on the economic impact of the trade deal from the U.S. International Trade Commission within 105 days after the agreement is signed (which would be in mid-March 2019 if the parties sign the deal at the end of November 2018). Republicans in Congress are considering trying to pass the bills in 2018 during a lame duck session of Congress, but it is not certain that the ITC report would be available that quickly. The Congress could vote to modify the rules and not require the ITC report for passage to meet a more aggressive timeline. Without strong bipartisan support for the deal, the normal timeline is more likely, and the 116th Congress that takes office in January 2019 will likely be the one that considers the agreement.

Figure 2: USMCA Timeline Under Trade Promotion Authority

Source: Congressional Research Service

What does it all mean?

The new agreement confers a degree of stability to automotive production in North America that could increase North American light vehicle content on the margins – particularly for “core parts” (engines, transmissions, body & chassis, axles, steering, suspension, and advanced batteries). There is a new six-year review process that is, in essence, a 16-year sunset clause if the parties do not come to a new agreement on any unsettled issues during the periodic review – but all of that is better for the stability of the North American industry than either a NAFTA pull-out or a bi-lateral U.S.-Mexico deal. Most vehicles produced in the United States and Canada either already meet the new rules or are close to meeting the new rules, and, as mentioned previously, roughly 68 percent of current Mexican vehicle production is already conforming. What’s more, automakers sell 82 percent of their U.S. automotive production in the U.S. market; since these vehicles never leave the country, they are not subject to any trade agreement content rules. That means the new rules mostly impact Mexican produced light vehicles and parts, as well as non-North American parts content used in U.S.-, Canadian-, and Mexican-built vehicles.

Figure 3: Sales of U.S. Produced Light Vehicles by Automaker National Origin, 2017

Source: CAR analysis of IHS|Markit data

*Japan includes Renault-Nissan-Mitsubishi

The USMCA coupled with the threat of Section 232 tariffs on non-North American imports will incentivize automakers and suppliers to move more work to the region. Conforming to the USMCA rules and strategic responses to avoid the risk of additional tariffs will raise production costs for light vehicles and automotive parts, driving up consumer prices. With peak automotive sales in 2016, the United States is in the wrong part of the business cycle for automakers and suppliers to consider making substantial new investments to re-shore production or expand operations in the United States. The Section 232 auto and parts tariffs are not yet in effect. However, the EU and Japan have won a reprieve from the impact of the tariffs while they work to negotiate new trade deals with the United States. If the EU and Japan deals lead to a more long-term exemption such as the ones negotiated by Canada and Mexico, the overall impact of these potential tariffs will be greatly diminished. Most of the USMCA rules have a three-year transition period, and if all goes smoothly in the three countries’ ratification process, the target effective date is 1 January 2020.

The current Section 232 steel and aluminum tariffs and the ongoing Section 301 trade dispute with China is already raising prices for consumers and suppliers – including those that rely on domestically-sourced inputs due to increased demand for these sources. A Section 232 auto and parts tariff that exempts Canada and Mexico is better for the U.S. auto industry than one that does not. However, the potential for there to be even more tariffs – or even a higher U.S. MFN rate – will likely cause changes in the North American industry. CAR’s preliminary analysis of the imposition of Section 232 tariffs shows that widespread imposition will be a net negative for the U.S. industry, the overall economy regarding employment and gross domestic product, and will raise consumer prices even further.