The fourth round of North American Free Trade Agreement (NAFTA) negotiations between the United States, Canada, and Mexico began October 11, 2017 in Washington, D.C. So far, the previous rounds of negotiations have produced little progress on the issues of greatest concern to the automotive industry, and this slow pace of resolving issues on the table calls into question the prospect of wrapping up negotiations by the end of the calendar year. This article provides an update of the negotiations to date, and what to expect with regard to the major issues in the talks.

Rules of Origin

Rules of Origin (ROO) are one of the thorniest NAFTA issues for the automotive industry. Currently, NAFTA contains a 62.5 percent threshold for Regional Value Content (RVC) in motor vehicles and parts, which is the highest ROO of any U.S. trade agreement. The Trump Administration has recently proposed:

- Raising the NAFTA RVC to 85 percent,

- Requiring 50 percent U.S. content as part of the 85 percent RVC,

- Including all parts, components, and materials in a light vehicle to “modernize” the tracing list, and finally,

- Instituting a validation process for content, rather than the current process whereby manufacturers can “deem originating” for parts, components, and vehicles produced within the NAFTA region.

The intent of tracing is to prevent manufacturers from “rolling up” imported content that originates from outside North America. In other words, an engine assembled in one of the three NAFTA partner countries that contains non-NAFTA parts or components would not be considered 100 percent NAFTA originating; the non-NAFTA value must be subtracted from the total value. Currently, only items on the tracing list must be accounted for, and everything not on the list is “deemed originating.” Figure 1 is an overview of what parts and components are currently on the NAFTA tracing list.

Figure 1: What is on the NAFTA tracing list

Secretary of Commerce Wilbur Ross has repeatedly criticized the NAFTA tracing list for being “out of date.” While the NAFTA tracing list does include some parts that are not found in many modern automobiles (including distributors and cassette decks), there are very few modern car and truck parts or components for which there is a motor vehicle-specific Harmonized Tariff Schedule (HTS) code that are NOT on the NAFTA tracing list. Figure 2 displays some of the parts and components of modern cars and trucks for which there is no vehicle-specific HTS code.

Figure 2: What is not on the NAFTA tracing list

The inclusion of materials and all motor vehicle parts and components would change the rules of the game for trading using the NAFTA preference. Already, there are differences in RVC levels between cars (that often have lower NAFTA content due to global platforms and global supply chains) and CUVs/SUVs/trucks (that often have higher NAFTA content due to regional production and supply chains). Auto manufacturers could decide that the higher RVC threshold and the proposed validation process is too costly, and that it would be less costly to eschew the NAFTA preference for the 2.5 percent Most Favored Nation (MFN) tariff on motor vehicles and parts imported to the United States. Importing vehicles, parts, and components under MFN tariffs opens up the supply chain to countries beyond NAFTA, and could result in lower overall NAFTA content in vehicles produced in Canada, Mexico, and the United States. In 2016, 94.7 percent of U.S. imports from Canada were traded using the NAFTA preference, and 87.6 percent of motor vehicles, bodies & trailers, and parts from Mexico utilized the NAFTA preference, as shown in Table 1 below.

Table 1: 2016 U.S. Motor Vehicle, Bodies & Trailers, and Parts Imports from Canada and Mexico by Trade Program

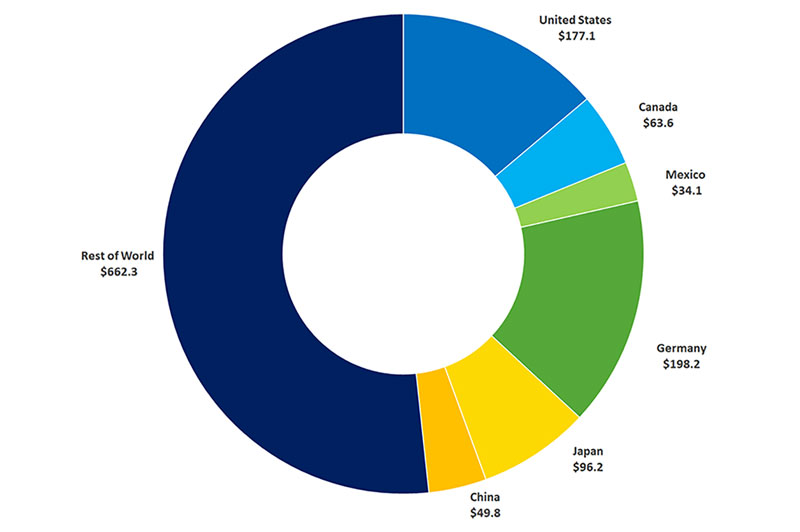

In a September 21, 2017 opinion piece in The Washington Post, Secretary Ross claimed that U.S. content of Canadian and Mexican vehicle imports is much lower than some analysts have previously claimed. Highlighting a Commerce Department analysis of OECD’s Trade in Value Added (TiVA) data written by U.S. Office of Trade and Economic Analysis Department staffers Ann Flatness and Chris Rasmussen, Ross claimed that the U.S. share of all manufactured goods imported from Canada has fallen from 21 percent in 1995 to 15 percent in 2011, and the U.S. share of all manufactured goods imported from Mexico has fallen from 26 percent to 16 percent in the same time period. The report states that the NAFTA share of U.S. motor vehicle imports has fallen from 46.4 percent in 1995 to 34.8 percent in 2011. It is true that the U.S. and NAFTA shares of U.S. vehicle imports have declined, but the overall value of trade has increased so that a smaller share may still represent a larger volume of trade—that is, the market pie is bigger. In 1995, total global motor vehicle trade was just $456.5 Billion; by 2011, it had grown 180 percent to 1.3 Trillion; and by 2016, total global motor vehicle trade was 197 percent larger than it was in 1995 at $1.4 Trillion. The U.S. portion of total global motor vehicle trade was $84.3 Billion in 1995; $177.1 Billion in 2011 (110 percent higher than in 1995); and $229.7 Billion in 2016 (172 percent higher than in 1995). The share decline during the period 1995-2011 reflects the growing economic participation of China and other growing economies—there are more pieces of pie.

Figure 3: The Changing Volume and U.S., Canada, Mexico, E.U., Japan, China, Rest of World Share of Motor Vehicle Trade

Trade in Passenger Vehicles (HS 8703): 1995 Billions of Dollars

Total of $456.6

Trade in Passenger Vehicles (HS 8703): 2011 Billions of Dollars

Total of $1,281.2

Trade in Passenger Vehicles (HS 8703): 2016 Billions of Dollars

Total of $1,354.5

It is also important to note that the TiVA data only includes vehicle trade, not parts or components. The Commerce Department study Secretary Ross cites also reports that in 2011, automotive imports to the United States from Canada contained 71.2 percent NAFTA content, and automotive imports from Mexico contained 70.5 percent NAFTA content—both well above the 62.5 percent RVC. It is also important to note that while 2011 is the most recent year for which TiVA data is available, a great deal has changed in the U.S. light vehicle market composition, automaker and supplier investments, and sourcing patterns since then. As shown in Figure 3, the total volume of motor vehicle trade has increased since 2011, as well.

A Poison Pill

While the Canadian and Mexican negotiating teams have many points of disagreement with the Trump Administration’s NAFTA bargaining positions, the U.S. proposal to include a “sunset clause” in the new agreement has drawn perhaps the sharpest rebukes from the trading partners, as well as from U.S. business groups including the U.S. Chamber of Commerce. The Administration has proposed a provision that would force a NAFTA renegotiation every five years—a move that would inject additional risk into any long-term manufacturing investment, production footprint, and supply chain sourcing decisions.

Timing

From the beginning, all three NAFTA countries have expressed the intent to expedite the NAFTA renegotiations to get out in front of next year’s Presidential elections in Mexico, Ontario Provincial elections in Canada, and the Congressional mid-term elections in the United States.

While “fast track” authority under the Trade Preferences Extension Act of 2015 technically expires July 1, 2021, there is a provision in the law that allows the U.S. Congress the opportunity to cancel the next three years of fast track authority prior to July 1, 2018. This means that the Congress could revoke fast track authority by next July, and this possibility puts additional pressure on negotiators to reach a deal on a revised NAFTA before next summer.

The Trump Administration’s move to place a 300 percent tariff on Canadian-built Bombardier aircraft in a trade dispute with Boeing could also alter the timeframe for negotiations. The United States claims that the aircraft are built with unfair subsidies from the Canadian government, and the U.S. action involves other countries since major parts of the airplane in question are built in Northern Ireland. The proposed duties do not go into effect unless affirmed by the U.S. International Trade Commission in early 2018. The aircraft dispute will hang over the NAFTA negotiations, and could impede the ability to reach an agreement on other aspects of trade between the United States and Canada.

What If Negotiators Do Not Reach An Agreement By The End of 2018?

There are three main options if the NAFTA negotiators do not reach a new agreement: the parties could continue to negotiate, knowing that there would be limited time to get the agreement approved in all three countries; the three countries could agree to continue trading under the existing agreement; or one or more parties could withdraw from NAFTA, effectively terminating the agreement.

The last option—terminating the agreement—is a very real possibility. The U.S. Congressional Research Service has written several reports that detail what could happen if NAFTA was terminated, and there are no clear-cut answers (Canis, Villarreal, & Jones, 2017), (Villarreal & Fergusson, The North American Free Trade Agreement, 2017), (Villarreal, U.S.-Mexico Economic Relations: Trends, Issues, and Implications, 2017), (CRS Reports & Analysis: Legal Sidebar, 2017). Trade dispute resolution mechanisms would disappear; the U.S. and Canada would have to decide whether to reinstate their previous bi-lateral trade agreement; and Congress would have to rescind NAFTA’s enabling legislation, and that in itself could be a tall order.

However, the most likely outcome, according to the Peterson Institute for International Economics (PIIE), is that the parties will “muddle through” with concessions on specific products and some “modernization.” PIIE researchers project that renegotiation will stretch beyond December 2017. What exactly those concessions will be, or what form “modernization” might take will be better known, but certainly not concluded from this round of negotiations. In short, no one “wins.” (Hufbauer, Jung, & Kolb, 2017).